How do you know if an account is debited or credited?

Debits are always on the left side of the entry, while credits are always on the right side, and your debits and credits should always equal each other in order for your accounts to remain in balance. In this journal entry, cash is increased (debited) and accounts receivable credited (decreased).

Debits are recorded on the left side of an accounting journal entry. A credit increases the balance of a liability, equity, gain or revenue account and decreases the balance of an asset, loss or expense account. Credits are recorded on the right side of a journal entry. Increase asset, expense and loss accounts.

All debit accounts are meant to be entered on the left side of a ledger while the credits are on the right side. For a general ledger to be balanced, credits and debits must be equal. Debits increase asset, expense, and dividend accounts, while credits decrease them.

A debit to your bank account occurs when you use funds from the account to buy something or pay someone. When your bank account is debited, money is taken out of the account. The opposite of a debit is a credit, in which case money is added to your account.

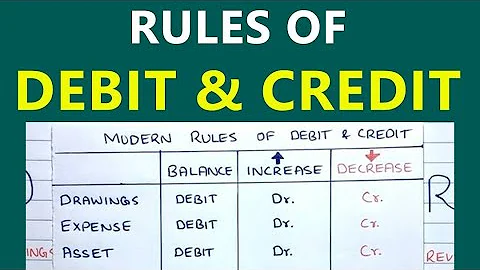

Tip. Debits are money going out of the account; they increase the balance of dividends, expenses, assets and losses. Credits are money coming into the account; they increase the balance of gains, income, revenues, liabilities, and shareholder equity.

The balance on an asset account is always a debit balance. The balance on a liability or capital account is always a credit balance. (Later on in this section you will learn how to work out the final or closing balance on an account which has both debit and credit entries.

Each transaction will include the date you made the transaction, a description of the transaction and the value. It will also include any credits into your account, such as Credit Card bill payment you may have made or a refund you may have received. These will be marked with a 'Cr' next to the amount.

Rules for Debit and Credit

The following are the rules of debit and credit which guide the system of accounts, they are known as the Golden Rules of accountancy: First: Debit what comes in, Credit what goes out. Second: Debit all expenses and losses, Credit all incomes and gains.

A Mathematical Understanding of Debits & Credits

A simple way to distinguish between the two is to know that a debit entry always adds a positive number to the ledger, and a credit entry always adds a negative number.

Debit represents the left side of an account and denotes an increase in assets and expenses or a decrease in liabilities and equity. Credit represents the right side of an account and denotes an increase in liabilities and equity or a decrease in assets and expenses.

Which of these account is debited?

Records that typically have a debit balance incorporate resources, losses, and expense accounts. Instances of these records are the cash account, debt claims, prepaid costs, fixed resources (assets) account, compensation, and salaries (cost) loss on fixed assets sold (loss) account.

Example of a Credit Balance

Bank Account: Jane has a checking account with her local bank. After depositing her paycheck, her account balance is $2,000. This is a credit balance, representing the amount of money Jane has available to spend or withdraw.

Thus, when the customer makes a deposit, the bank credits the account (increases the bank's liability). At the same time, the bank adds the money to its own cash holdings account. Since this account is an Asset, the increase is a debit. But the customer typically does not see this side of the transaction.

Debits increase asset or expense accounts and decrease liability, revenue or equity accounts. Credits do the reverse. When recording a transaction, every debit entry must have a corresponding credit entry for the same dollar amount, or vice-versa. Debits and credits are a critical part of double-entry bookkeeping.

Debits (often represented as DR) record incoming money, while credits (CR) record outgoing money. How these show up on your balance sheet depends on the type of account they correspond to.

The most important point to remember is the DEBIT literally means LEFT and CREDIT literally means RIGHT. Let's take a look at one more example, also from NeatNiks.

Cash payment received on an account receivable: Cash account is debited and accounts receivable is credited. Supplies purchased from a supplier for cash: The supplies expense account is debited and the cash account is credited. Payroll for employees: The payroll tax accounts are debited and the cash account is credited.

(1) A “credit transaction” is a transaction under which one party (“the creditor”)– (a) supplies any goods or sells any land under a hire-purchase agreement or a conditional sale agreement, (b) leases or hires any land or goods in return for periodical payments, or.

A cash transaction refers to an immediate exchange of physical currency for goods or services. It involves the direct payment in cash at the time of purchase. A credit transaction is a delayed payment method where goods or services are received upfront, and the payment occurs at a later date.

A debit transaction is a point of sale purchase that is processed using a bank card linked to a checking account. Unlike a credit transaction, a debit transaction usually requires that the customer have the money available in their bank account to cover the transaction.

What is the 3 golden rules of accounts?

The three golden rules of accounting are (1) debit all expenses and losses, credit all incomes and gains, (2) debit the receiver, credit the giver, and (3) debit what comes in, credit what goes out. These rules are the basis of double-entry accounting, first attributed to Luca Pacioli.

When your bank account is debited, money is taken out of the account. The opposite of a debit is a credit, in which case money is added to your account. Your account is debited in many instances..

A left-sided entry is headed with debit. It increases an asset or expenses account or decreases equity liability or revenue accounts. For example, 'Purchase of a new computer. Here, the asset gained (computer) is to be notified on the left side of the asset account.

A debit is a record of the money taken from your bank account, for example when you write a cheque. The total of debits must balance the total of credits. Synonyms: payout, debt, payment, commitment More Synonyms of debit.

On a balance sheet or in a ledger, assets equal liabilities plus shareholders' equity. An increase in the value of assets is a debit to the account, and a decrease is a credit.